The opinions expressed in this blog are solely the author’s and do not reflect the views of PayPal.

By @Alexandros Bottenbruch

First dubbed the “Sick man of Europe” in the late 1990s following post-reunification struggles with high unemployment, sluggish growth, and steep integration costs, Germany was once again given this epithet in 2024.1 However, despite Germany’s economy entering its second year of recession and corporate insolvencies hitting levels last seen during the 2009 financial crisis, it remains the world’s third-largest economy (just ahead of China) and the beating heart of Europe’s industrial powerhouse.2 Understanding how macroeconomic forces, consumer behaviours, and emerging investment opportunities intersect is key to navigating this evolving landscape—and seizing the upside that comes with it.

Germany’s Economic Resilience & Structural Hurdles

Germany stands among the top three global exporters, bolstered by an industrial sector that accounts for roughly 27% of gross value added—the highest in the “Group of Seven” (G7), which also includes Canada, France, Italy, Japan, the United Kingdom, and the United States.3 While other countries pivoted heavily toward services, Germany’s industrial core remains a defining competitive advantage.4,5

At the heart of this competitive edge is the Mittelstand (Germany’s network of predominantly small to medium-sized, family-owned firms), widely renowned for engineering excellence and niche-market leadership. Nearly 1,000 of these companies are considered “hidden champions,” excelling in specialized segments worldwide.6 However, structural pressures—including high energy, labor, and tax costs; complex regulations; waning Chinese demand; and past reliance on Russian energy—are weighing on growth and business confidence, especially with business insolvencies surging 38% year-over-year in 2024.7,8

Still, Germany’s industrial muscle, engineering know-how, and powerful business networks remain formidable assets.

Consumer Behaviour – Caution Defines Financial Habits

Germany may be the world’s third-largest economy, yet it ranks only 17th globally in per-capita financial assets (€95K vs. €315K in the US). This disconnect can be largely attributed to Germany’s longstanding preference for saving over investing; while North America attributes roughly two-thirds of wealth growth to market appreciation, Germany’s pattern is nearly the opposite—accumulation is driven almost entirely by savings. This conservative stance towards investing has been shaped by historical episodes of financial upheaval, from memories of hyperinflation to more recent setbacks. These include the 1990s Deutsche Telekom “Volksaktie” — a state-promoted retail investment wave that ended in disillusionment — and the collapse of the “Neuer Markt,” a tech-focused exchange segment that mirrored the dot-com crash.9 When these government-backed initiatives ended in substantial losses for many retail investors, it further solidified a deep-seated scepticism toward equities.10

Today, this cautious mindset is reflected in the prevalence of low-risk products—like savings accounts, life insurance, and fixed-income investments—over stocks or alternative assets. Unsurprisingly, the products and services that resonate most with German consumers and businesses revolve around trust, reliability, and steady returns—rather than the promise of outsized gains.

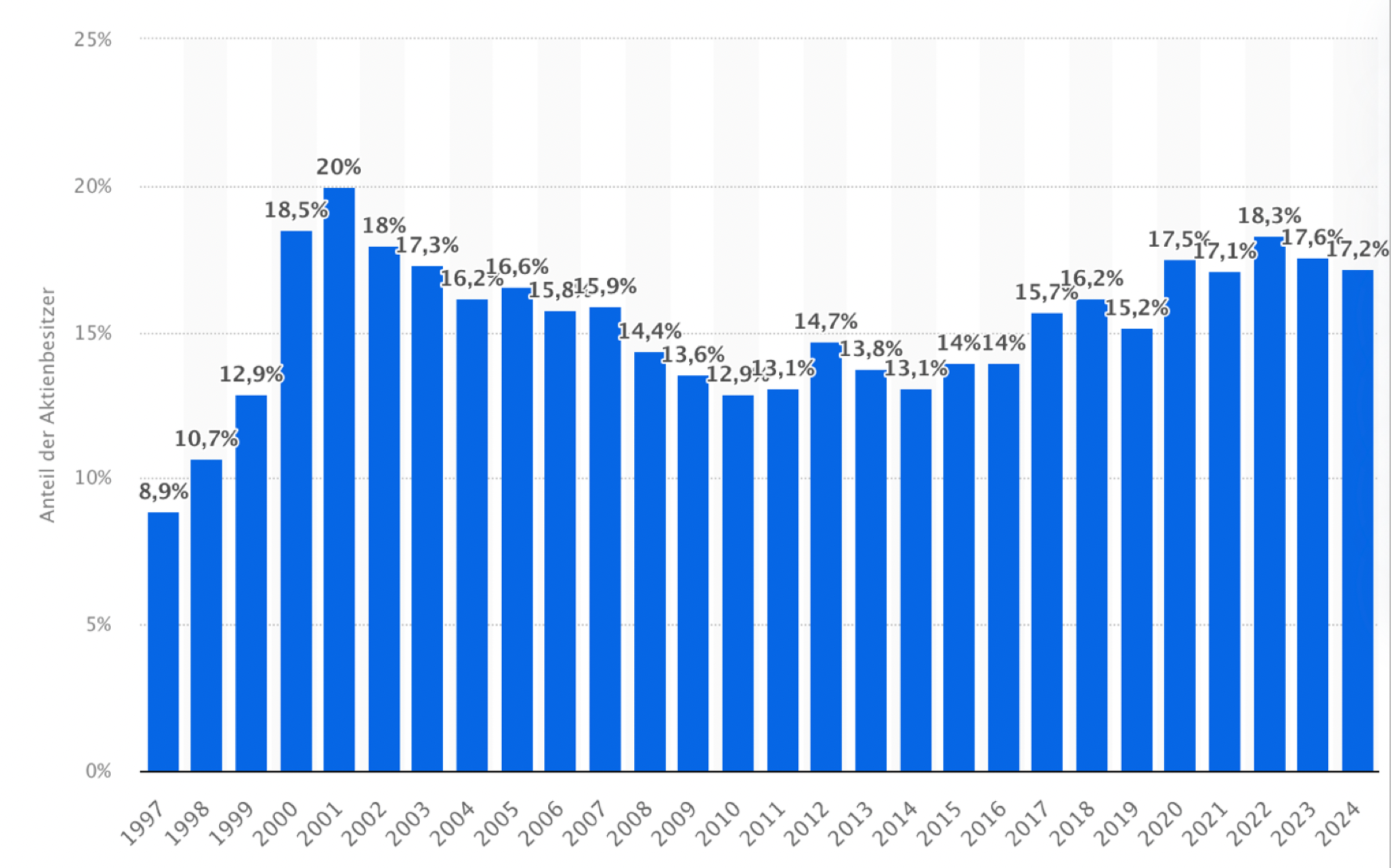

Fun fact: 83% of German households own personal liability insurance (21% in the U.S.), 46% legal protection insurance (6% in the U.S.) and 42% accident insurance (21% in the U.S.), while only 17.2% of Germans are invested in equities (62% in the U.S.)11,12

Equity Ownership as a % of the Total Population in Germany (1997 to 2024)

Source: Statista 2025 (here)

Venture in Germany: Where Industrial Heritage & Cautious Habits Drive Innovation

Against the backdrop of Germany’s robust economic fundamentals, deep industrial DNA, and cautious financial habits, we see a distinctive environment shaping up where innovation flourishes. Enterprise software—particularly industrial and supply-chain solutions—has garnered the most capital since 2020 ($10.2B), followed by fintech ($9.5B), transportation, leveraging Germany’s automotive legacy ($7.8B), and energy, driven by a renewed focus on energy independence ($7.3B).13,14

Digging deeper into fintech investments, Germany’s industrial backbone—especially its Mittelstand—has profoundly influenced the ecosystem, driving demand for financial solutions that streamline manufacturing, logistics, and supply chain workflows. As a result, much of the country’s fintech innovation is B2B, from supplier payments to invoice factoring, while consumer-centric fintech also continues to thrive serving Mittelstand and German consumers by embracing a partnership-based approach—offering niche services on top of incumbents’ foundations rather than seeking outright disruption. This strategy better aligns them for success in a country where established institutions and a cautious approach to novel tech solutions remain the norm.15

With German consumers still gravitating toward security and savings, fintechs that package safe, user-friendly products or insurtech solutions are finding growth opportunities. Meanwhile, established banks’ reliance on costly legacy operations opens the door for challenger models that deliver more efficient, digital-first experiences, and alternative lending offerings. Although AI in finance remains in its infancy, the “green shoots” are visible—and early movers who effectively navigate Germany’s regulatory maze could establish a strong foothold.

Staying Bullish: Our Investor Take on Germany’s (Fintech) Future

Despite Germany’s often risk-averse culture and stringent regulatory framework, these very conditions can pave the way for transformative fintech innovations—especially in regtech and partnership-based financial services. Demand for cost-efficient, digitally driven solutions continues to expand across one of Europe’s most robust economies, forming the backbone of our long-term bullish view on Germany’s fintech sector.

The recent federal elections, with voter turnout hitting 82.5%—the highest in 38 years—underscore Germany’s dynamic democratic engagement but also reveal deepening political polarization. While the far-right Alternative for Germany (“AfD”) surged to 20.8% and the center-left Social Democrats (“SPD”) hit a historic low of 16.4%, far-left parties collectively amassed nearly 14%—though one narrowly missed the 5.0% threshold for parliamentary representation. Together, these outcomes signal an imperative for the incoming coalition (the center-right Christian Democrats (“CDU/CSU”) that garnered 28.5% and SPD) to deliver meaningful reforms that restore public confidence and stimulate economic growth.

Notably, the CDU of today differs from the party under Angela Merkel—whose background as a trained quantum chemist and formative years in the former East Germany (DDR) shaped her pragmatic leadership style for 16 years. By contrast, Friedrich Merz—a veteran of corporate boardrooms and finance—reflects a return to more liberal, pro-business policies, a shift greeted by technology founders and the wider business community as a timely chance to rekindle growth and curb disillusionment.

On April 9, 2025, CDU (conservatives) and SPD (social democrats) concluded their coalition negotiations. The new Federal Government under Chancellor Friedrich Merz (CDU) is expected to be more business friendly, as strengthening economic competitiveness as well as reducing bureaucracy and taxes are key priorities. The new government establishes a new Federal Ministry for Digitalization and Modernization to oversee and accelerate Germany's digital transformation and public sector modernization, which will be led by the CDU (Karsten Wildberger, the new minister served as CEO of a big German consumer electronics retailer) . Business representatives welcomed the swift agreement and important impetus and called for swift and decisive implementation.

Meanwhile, Germany’s solid fiscal position further reinforces its capacity for economic renewal. With the lowest debt-to-GDP ratio among the G7 (around 62.9%), the country’s constitutional debt brake (“Schuldenbremse”) has afforded it the discipline to allocate a €500 billion special fund (“Sondervermögen”) for infrastructure, defense, and investment. This provides Germany with flexibility that many advanced economies lack, and if focused on appropriate initiatives, it could stimulate innovation across various sectors—including fintech.

Among Germany-based tech founders, optimism is building—alongside the conviction that the moment for decisive action is now. As leading SaaS and fintech entrepreneurs emphasize, the government must follow through on pro-business commitments or risk fueling disillusionment on both ends of the political spectrum. For fintech investors, this is both a challenge and an opportunity: while progressive policies could unleash new waves of innovation, any failure to deliver would undermine the very core of Germany’s social market economy (“soziale Marktwirtschaft”), which relies on a strong, inclusive economy. Yet the country’s industrial heritage, deep engineering expertise, and evolving political landscape all point toward an auspicious setting for forward-thinking ventures willing to navigate this transformative chapter in Germany’s story.

PayPal Ventures Investments in Germany

With the industrial backbone and evolving consumer needs in mind, our own Ventures portfolio reflects a blend of B2B and consumer-focused approaches that tap into Germany’s distinct market dynamics.

PPV’s investment portfolio in Germany covers areas ranging from payment aggregation and orchestration tools (PPRO), B2B payment platforms serving Germany’s Mittelstand (Pliant), vertical SaaS provider catering to Germany’s automotive industry and Mittelstand (via car dealerships) (Aufinity), to leading consumer fintechs that empower individuals to have a 360-degree view of their personal finances (Finanzguru), while also optimizing their savings yield (Raisin).

See Appendix I for an overview of PayPal Ventures’ German fintech portfolio and Appendix II for an overview of other notable fintech players (consumer-fintech-biased view) in the ecosystem.

The Next Frontier

There’s a real opportunity here, but also a narrowing window to capture it. As customer expectations shift and the market keeps evolving, we expect that the companies that move decisively, automate where possible, and build around their users will come out ahead. AI and agent-powered workflows are raising the bar for what “efficient” and “seamless” actually look like.

Appendix I – PayPal Ventures’ Fintech Investments in Germany

|

Company

|

Description

|

|

Raisin

(initially invested in 2017)

|

Consumer Fintech.

Online savings (deposit rate and investment product) marketplace.

1M+ customers / >€70B in AUM

|

|

PPRO

(initially invested in 2018)

|

Payments.

Europe’s largest Alternative Payments Methods (“APM”) aggregator [APMs typically account for 20-30% share of checkout in ecommerce in EU member states, and can go as high as 70% in countries like Netherlands].

|

|

Finanzguru (initially invested in 2023)

|

Consumer Fintech.

Open-banking powered financial advisory that enables consumers to connect all their bank accounts via open banking, get an automated overview of all their contracts / subscriptions / insurances, and see personalized money saving / budgeting tips.

Monetization via insurance brokerage commissions and subscription products.

|

|

Aufinity

(initially invested in 2024)

|

Vertical SaaS / embedded finance.

Operates an automotive (car dealership-focused) vertical SaaS and payment management platform in Germany, Italy, and Spain.

Monetization via SaaS subscription and transaction-driven (including payment) revenues.

|

|

Pliant

(initially invested in 2024)

|

B2B payments.

Specializes in corporate credit card solutions tailored for businesses across Europe. Enables companies to issue both physical and virtual cards, streamline payment processes, monitor expenditures in real-time, and integrate seamlessly with existing accounting systems.

|

Note: In this Appendix, references to other investors is non-exhaustive.

Source: PitchBook, Company Websites, Company Press Releases

Appendix II – Non-Exhaustive List of Other Notable Fintech Startups in Germany

|

Company

|

Description

|

|

Bling.de

(founded in 2021)

|

Consumer fintech.

Europe’s first super-app for families that provides an easy-to-understand, family-friendly digital solution that helps educate and simplify families‘ lives in the areas of savings, investments, communications, and security.

|

|

Lemon Markets

(founded in 2020)

|

Brokerage infrastructure.

Provides infrastructure that allows companies to launch an investment product and brokerage API combined with operational capabilities (order execution) and regulatory know-how to power stocks, ETFs, etc. capabilities.

|

|

Liqid

(founded in 2015)

|

Consumer fintech.

Digital wealth management spanning public and private (private equity, real estate, and venture capital funds) assets. Minimum €100K+ in investable assets.

€3B+ in AUM // 10K+ clients

|

|

Moonfare

(founded in 2016)

|

Consumer fintech.

Developer of an investment platform designed to facilitate private market investing for wealthy individuals across private equity, venture capital, and other institutional investor opportunities through feeder funds.

Co-founded by former Head & MD of KKR Germany and ex-McKinsey Partner / N26 Product Leader.

€3.3B in AUM // 70K+ members // 20+ countries

|

|

N26

(founded in 2013)

|

Consumer fintech (fully-licensed bank).

Digital (neo)banking platform and provider of financial services ranging from current accounts, financing, consumer credit, to investments such as savings and crypto trading, enabling users to manage and control their banking details digitally.

Est. FY24 revenues of €440M (+40% YoY), turned operationally profitable (€2.8M in 3Q24).

€10B in deposits // 4.8M revenue-relevant customers

|

|

Scaleable Capital

(founded in 2014)

|

Consumer fintech.

Operator of a digital wealth management platform designed to simplify investment decisions.

€20B in AUM (as at 4/2024) with 2/3 of assets invested in ETFs (1M+ monthly ETF / stock savings plans)

|

|

Trade Republic

(founded in 2015)

|

Consumer fintech.

Originally founded as an investing brokerage platform (comparable to Robinhood) – has since evolved to become Europe's largest savings platform.

Acquired a full banking license from the ECB in 12/2023.

€100B+ AUM // 8M+ customers // 15+ countries

|

|

UnitPlus

(founded in 2021)

|

Consumer and B2B fintech.

Initially positioned as the first capital market bank to give consumers safe and simple access to investment markets; now evolved to also serve SMEs with a modern cash management solution (in partnership with Goldman Sachs Asset Management).

|

|

Upvest

(founded in 2017)

|

FinTech Infrastructure.

Developer of an investment API designed to empower financial institutions to offer investment products in their app with a modular, scalable, and accessible alternative leveraged by leading consumer fintech platforms, including Revolut, N26, Raisin, vivid, and plum.

|

Note: In this Appendix, the identification of investors is non-exhaustive.

Source: PitchBook, Company Websites, Company Founders, VCs invested in respective assets.

Appendix III – Breakdown of Economic Activity by Sector

Source: World Bank

Appendix IV – Ranking of leading industrial economies’ attractiveness

Appendix V – The Digital Economy & Society Index (DESI) – 2022

Appendix VI – IT Investments as a % share of GDP

-

1 For context, the term "Sick Man of Europe" was first popularized in the context of Germany in the late 1990s by The Economist, reflecting Germany's economic struggles post-reunification, characterized by high unemployment and sluggish growth. The epithet resurfaced in 2024, highlighting ongoing economic challenges, including the impacts of the COVID-19 pandemic and energy crises, which have further strained Germany's industrial sector.

-

2 Germany’s Federal Foreign Office (Deutschland.de)

-

3 World Bank Data, Santander Trade Markets – Research: Germany: Economic and political outline

-

4 Santander Trade Markets – Research: Germany: Economic and political outline

-

5 Economic Key Facts Germany (as of February 2025) by KPMG

-

6 Germany’s Federal Foreign Office (Deutschland.de)

-

7 Reuters 12/27/2024 article titled “German business associations pessimistic about 2025, IW says”

-

8 Reuters 1/9/2025 article titled “Germany records highest company insolvencies since financial crisis”

-

9 Tagesschau article titled “Die Deutschen investieren schlecht“ (Germans invest poorly)

-

10 Allianz Global Wealth Report 2024: Surprising relief

-

11,12 Source: Statista (see here)

-

13 Note: Fintech in the context of all Dealroom statistics includes insurtech, crypto/DeFi, and fintech-focused regtech

-

14 Dealroom Guide on Germany (here)

-

15 Accenture’s Global Banking Consumer Study 2022 (here) found that 38% of U.K. consumers had their primary bank account with neobanks compared to 28% in Germany. German consumers citing data security, brand recognition and branch access as top factors for remaining with incumbents